STMicroelectronics : The Physical Efficiency Engine of the AI and Space Era

With the AI buildout exposing severe physical bottlenecks—power delivery, data movement, thermal limits—and orbital networks scaling into vital commercial infrastructure, a select group of companies is emerging as structural beneficiaries.

While the market chases hype-driven, single-variable infrastructure plays, STMicroelectronics (ST) has quietly embedded itself across the entire physical architecture of next-generation computing and connectivity.

From the high-voltage grid connection to the edge node and low-Earth orbit, ST is the physical efficiency engine running through the next-generation stack.

Let’s dive.

Three Decades of Sovereign Silicon

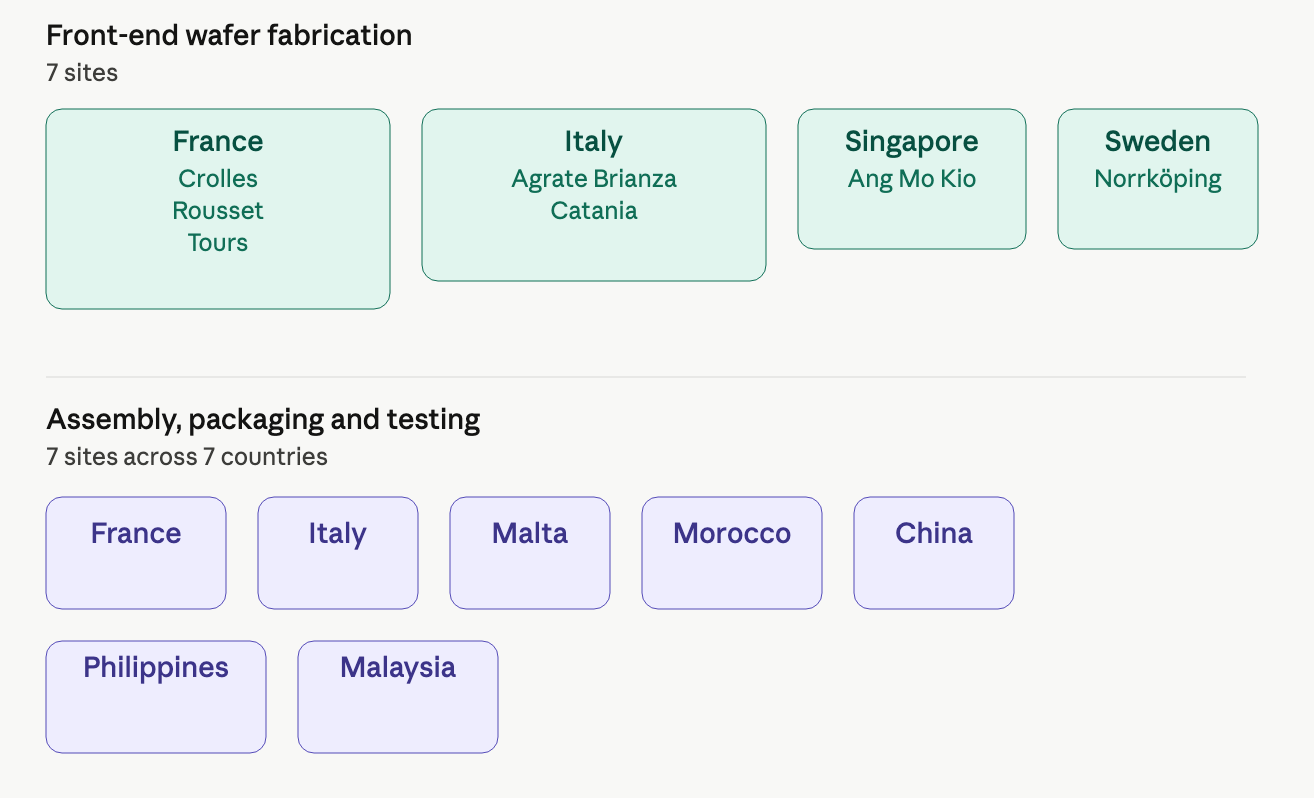

STMicroelectronics was born in 1987 from the merger of Italy’s SGS Microelettronica and France’s Thomson Semiconducteurs, inheriting a manufacturing footprint across Catania, Grenoble, Crolles, and Tours. In the fabless era that followed, owning factories appeared to be a structural disadvantage. Today it is one of the company’s clearest strengths.

Headquartered in Geneva, Switzerland, and employing close to 50,000 people across 12 manufacturing sites, ST is one of the last fully vertically integrated semiconductor companies in the Western hemisphere. As a pure-play Integrated Device Manufacturer (IDM), ST internalizes the entire product lifecycle: designing, fabricating, packaging, and directly distributing its own silicon.

In a technology landscape that has systematically outsourced physical production to East Asia, this sovereign manufacturing model is increasingly rare — and increasingly valuable.

STMicroelectronics — global manufacturing footprint :

This localized capital asset base serves a dual strategic function :

Operationally, it insulates ST from cross-strait geopolitical supply shocks while guaranteeing structural capacity to tier-one clients.

Technologically, it permits the in-house development of highly customized, proprietary manufacturing processes, capabilities an external foundry cannot replicate on someone else’s behalf.

Historically, ST’s revenue is built around four end markets:

Automotive: EV powertrains, advanced driver-assistance systems (ADAS), and localized body electronics.

Industrial: Factory automation, precision motor control, and power management infrastructure.

Personal Electronics: Premium smartphone sensor content and specialized low-power peripherals.

Communications Equipment: Hyperscale data center components, 5G infrastructure, and carrier-grade networking.

Across all four, ST maintains a diversified catalogue of products that touches the components and physical infrastructure of nearly every industry on Earth.

Understanding what sits inside that catalogue is the starting point for understanding why the company is structurally positioned for the AI era.

The Product Catalogue

Analog, MEMS and Sensors (AM&S)

ST’s largest segment gives devices their senses — the ability to detect motion, sound, pressure, distance, and temperature. The accelerometer that rotates your phone screen, the gyroscope in your car’s stability system, and the barometer in your smartwatch are all ST components.

The ISPU (Intelligent Sensor Processing Unit), ST’s latest-generation smart sensor, integrates a processor directly inside the sensor node itself, enabling autonomous equipment monitoring and predictive maintenance without waking the main chip. This is edge AI : intelligence embedded directly at the point where data originates.

In February 2026, ST closed the $950 million acquisition of NXP’s MEMS sensors business, adding the market-leading position in automotive safety sensors — airbag triggers, vehicle dynamics systems, tyre pressure monitoring — to its existing portfolio. For ST, sensors are core to its efficiency engine thesis, and NXP’s portfolio fills the last meaningful gap in its sensing coverage. The acquired business carried margins above ST’s corporate average and was immediately accretive.

Embedded Processing (EMP)

These are the brains inside devices — chips that run programs and control what a device does.

ST’s STM32 microcontroller family is the world’s most widely used 32-bit microcontroller by developer count, embedded in industrial automation, medical devices, consumer appliances, automotive ECUs, and factory robotics.

Market research firm Omdia has ranked ST as the number-one global vendor for general-purpose microcontrollers for five consecutive fiscal years.

In this segment, ST has an extraordinary economic moat: its developer ecosystem. Millions of embedded engineers have spent nearly two decades building software libraries, custom firmware, and proprietary toolchains around the STM32 architecture, creating prohibitive switching costs.

The new STM32N6, launch in 2026 aims to transforms this installed base into an AI asset. Its Neural-ART Accelerator delivers 600 billion operations per second on-chip, giving the existing ecosystem the ability to run machine learning locally without cloud dependency. Developers use tools to compress trained AI models small enough to run on a microcontroller consuming milliwatts of power — reducing latency, improving security, and enabling real-time responses for physical applications.

This is the edge AI capability ST is developing in direct collaboration with Nvidia, specifically to accelerate Physical AI: intelligence embedded in the robots, cameras, and industrial systems of the next automation age.

Power and Discrete (P&D)

Every watt of energy that enters a data center, an electric vehicle, or a solar installation must be converted from one voltage to another without wasting it as heat.

ST’s power chips perform this conversion — and doing it efficiently is one of the central engineering challenge of the AI era.

The flagship technology is Silicon Carbide (SiC). Conventional silicon struggles above 600 volts, losing too much energy as heat. SiC handles voltages up to 1,700V with far less loss, switches faster, and operates at higher temperatures — making it essential for EV traction inverters and for the 800-volt DC power architectures that AI data centers are adopting.

ST’s 800V DC portfolio is purpose-built for AI data centers, addressing the efficiency requirements that grow more critical with every new generation of GPU.

The Catania campus in Sicily is the world’s only fully integrated SiC facility, growing its own crystals from raw powder through to finished power modules on a single campus. No Western competitor has replicated this structure.

The segment also covers GaN transistors for high-frequency power conversion, conventional MOSFETs and IGBTs for motor drives and industrial automation, and thyristors for home appliances. ST views this power efficiency leadership not just as a commercial opportunity but as a strategic contribution to a lower-carbon industrial economy — the same technologies that make AI data centers more efficient also enable electric mobility and renewable energy conversion at scale.

This external sustainability drive aligns with ST’s internal commitments to be carbon neutral by 2027, anchored by a mandate to source 100% renewable electricity by 2027 (up from 86% achieved in 2025).

RF and Optical Communications (RFOC)

The smallest segment by revenue but the fastest-growing and highest-margin in 2026. These chips manage how devices communicate — at speeds copper cannot reach, over distances radio cannot span efficiently, and in environments where conventional silicon cannot survive.

The PIC100 silicon photonics platform moves data using light rather than electricity, enabling the 1.6 terabit-per-second optical connections that link GPU racks in AI data centers. It is in high-volume production on 300mm wafers — the only pure-silicon photonics platform at this scale in the world — and underpins a multi-year, multi-billion-dollar engagement with Amazon Web Services. AWS has committed not just commercial capacity but part of its financial balance sheet to ST’s optical roadmap.

The space chip business supplies approximately 90% of the LEO satellite semiconductor market, including Starlink, with radiation-hardened chips engineered to survive cosmic radiation.

AI Physical Crises and why ST is Indispensable

We all know by now that software-driven artificial intelligence revolution is running directly into hard physical limits.

And the sheer velocity of compute scaling has exposed three systemic crises within the physical layer of technology:

Power delivery inefficiencies.

The structural failure of copper networking.

Intelligence pushed to the edge cannot depend on cloud round-trips for latency-sensitive decisions.

ST’s deep-tech product roadmap addresses these exact bottlenecks, creating a series of structural moats :

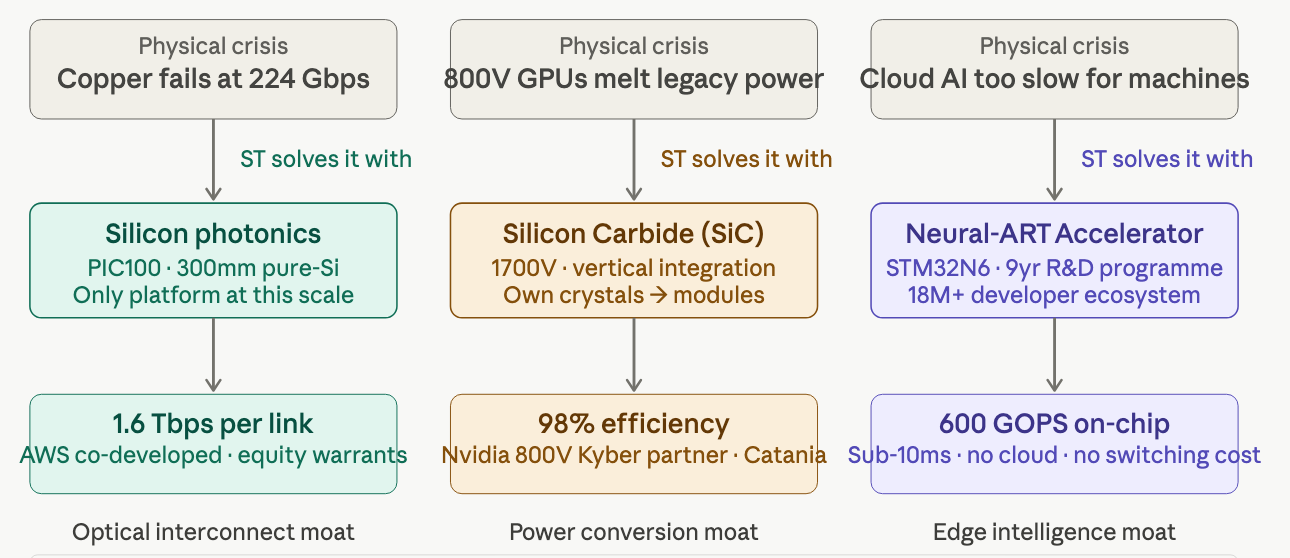

Silicon Carbide — The Power conversion

At the core of every AI data center lies a simple but unforgiving challenge:

Converting grid electricity into the ultra-low voltages required by GPUs, efficiently and at massive scale.

As power demands rise, conventional silicon begins to fail. Beyond roughly 600 volts, losses increase sharply and heat becomes difficult to manage.

Silicon Carbide offers a step-change improvement. It can operate at voltages up to 1,700 volts, with significantly lower energy loss, faster switching speeds, and higher thermal tolerance. This makes it uniquely suited for the 800-volt power architectures now being adopted in next-generation data centers.

ST recognized this shift early, investing in SiC as far back as 2016. Its Catania facility in Sicily is today the only fully integrated SiC manufacturing site in the Western world, covering the entire process from raw crystal growth to finished power modules.

The true corporate moat is structural and geopolitical. While competitors rely on third-party merchant wafer suppliers, ST’s Catania facility controls the raw substrate material stack.

Furthermore, SiC production relies exclusively on silicon and carbon — raw materials that are universally accessible. With China governing approximately 98% of primary global gallium supply and actively leveraging export restrictions that have driven merchant Gallium Nitride (GaN) material input costs up 30% to 50%, ST’s SiC-heavy strategy provides a highly supply-resilient power semiconductor architecture for the Western hemisphere.

While GaN is selectively retained for lower-voltage, high-frequency niches, ST’s core high-power roadmap is insulated from single-source geopolitical manipulation.

PIC100 photonics - The optical interconnect

As AI workloads scale, data centers are running into another hard limit: copper interconnects. At speeds of 224 Gbps, electrical signals degrade within a meter, making copper both inefficient and impractical for large-scale GPU clusters. The physics is clear — beyond a certain point, data must move as light, not electricity.

ST’s PIC100 silicon photonics platform addresses this constraint. Manufactured on advanced 300mm wafers, PIC100 achieves a decisive 2.3x chip yield multiplier per wafer compared to legacy 200mm foundry lines operated by competing pure-plays. This manufacturing advantage translates directly into cost, scalability, and supply reliability.

STM32 and Neural-ART — the edge intelligence

Beyond power and connectivity, the next frontier is where computation happens. The STM32 microcontroller family, introduced in 2007, remains the most widely adopted 32-bit microcontroller ecosystem in the world. Its strength lies not just in hardware but in the vast software ecosystem built by millions of developers over nearly two decades — switching costs are structurally prohibitive.

The latest STM32N6 generation extends this ecosystem into the AI era. Its integrated Neural-ART accelerator delivers 600 GOPS of on-chip performance, enabling real-time machine learning inference directly at the edge.

This shift is significant. Instead of sending data to the cloud for processing, devices can now analyze and act locally — whether in factory automation, medical imaging, or industrial sensing. The result is lower latency, improved reliability, and stronger data privacy.

This directly executes the strategy articulated by CEO Jean-Marc Chery during the Q1 2026 earnings call, positioning ST to supply the underlying hardware engineered to “power, cool, and connect AI data centers from the grid to the core and from the core to the user,” while securing capture of emerging AI-driven edge automation programs.

Architectural Integration: Across Six Layers of the AI Data Center

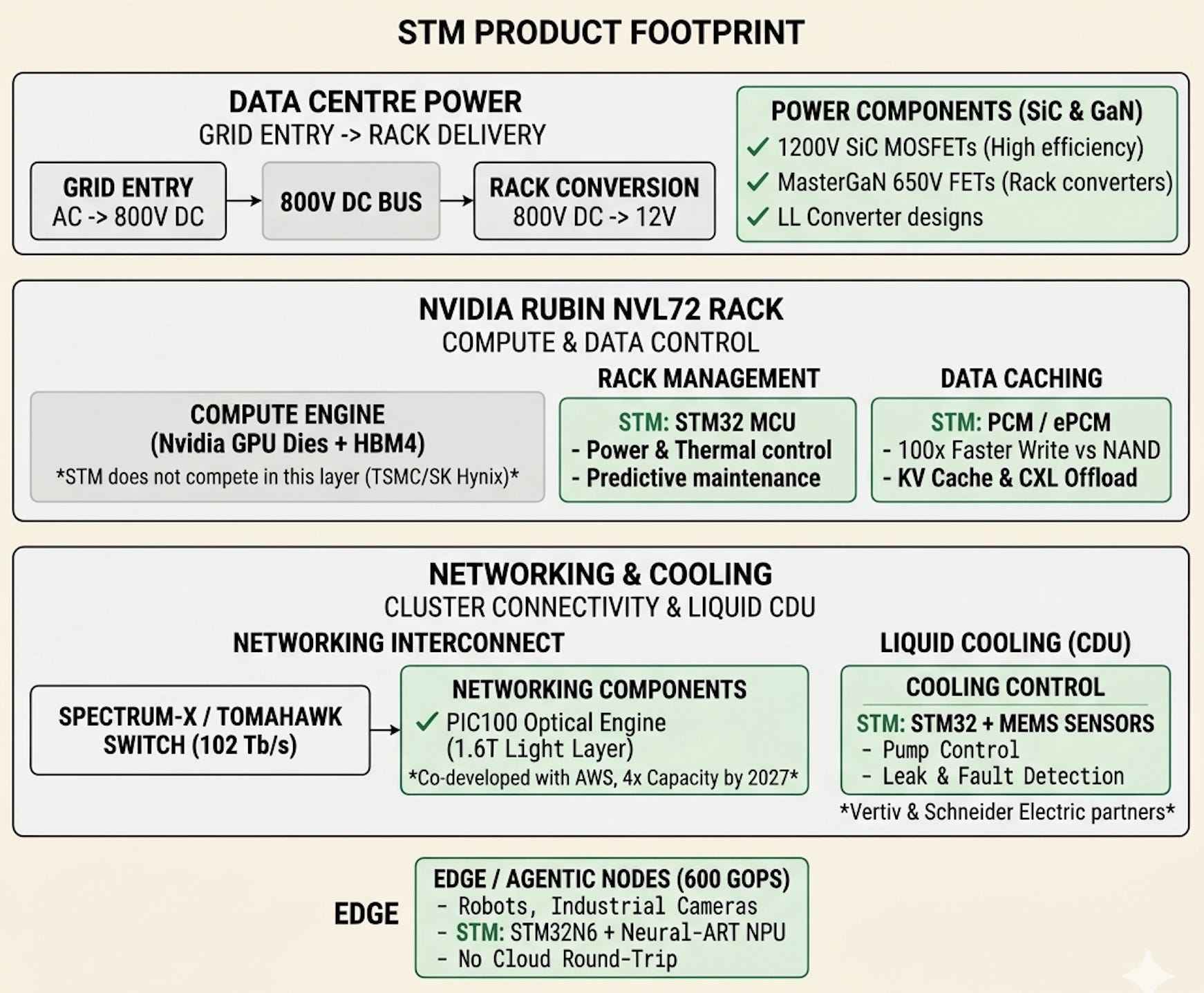

To appreciate the breadth of ST’s monetization model, one must move past viewing it as a component supplier and trace its systematic integration across six parallel physical layers of a single unified modern data center deployment, such as an Nvidia Rubin NVL72 architecture.

While Nvidia monopolizes the computational logic tier — designing the GPUs, advanced switch silicon, and high-level software frameworks — it relies entirely on merchant semiconductor architectures to construct the surrounding physical infrastructure.

ST’s multi-tier hardware portfolio populates these critical layers:

Layer 1: Grid Entry (High-Voltage AC to 800V DC) Utility power enters the facility as high-voltage AC electricity and must undergo immediate rectification. ST’s high-voltage SiC MOSFETs execute the primary step-down conversion into 800V DC — the standard distribution adopted across next-generation GPU. ST is integrated into these advanced reference designs as an official 800V silicon vendor, delivering co-developed conversion solutions operating above 98% efficiency.

Layer 2: Power Distribution (800V DC down to the Board) Once routed to the server rows, the 800V DC rail must be stepped down through intermediate stages toward localized board voltages. ST’s high-frequency GaN devices and specialized power management ICs (PMICs) govern these intermediate down-conversion stages, exploiting wide-bandgap switching velocities to minimize footprint and thermal dissipation.

Layer 3: The GPU Chassis (On-Board Control & Connectivity) Directly on the computing mainboard, STM32 microcontrollers serve as the low-level telemetry tier, continuously monitoring voltage regulation, rail health, and localized thermal behavior across dense accelerator arrays. Simultaneously, ST’s PIC100 silicon photonics engines anchor the optical transceivers, converting high-density electrical compute data into light to facilitate rack-to-rack clustering.

Layer 4: The Network Fabric (Switch-to-Switch Speed) At the network switch layer, ST’s PIC100 optical engines are integrated as co-packaged optics (CPO) directly alongside core routing ASICs designed by Broadcom and Nvidia. This multi-product integration validates management’s Q1 commentary that data center expansion is being driven by a diversified mix of cloud optical interconnects, advanced BiCMOS step-down arrays, and high-performance microcontrollers — rather than a single component exposure.

Layer 5: Thermal Management and Liquid Cooling Because high-density GPU configurations generate unprecedented thermal loads, modern data centers are migrating from ambient air cooling to closed-loop liquid cooling manifolds. Within these systems, ST’s automotive-grade MEMS sensors and dedicated microcontrollers govern the entire environmental safety tier: regulating high-pressure fluid pumps, mapping real-time flow dynamics, detecting microscopic fluid leaks, and executing predictive failure algorithms before thermal runaway can damage compute arrays.

Layer 6: Distributed Edge Infrastructure (Closing the AI Loop) Finally, the data center core connects directly to the edge environment, where ST’s STM32N6 microcontrollers run local computer vision and sensor inference. This layer feeds clean, pre-processed information back to the core cluster, closing the loop between centralized training and edge execution. This physical AI execution is reinforced by a strategic collaboration with Nvidia, designed to natively embed ST’s sensory and motor-control portfolios directly into the Nvidia robotics development platform.

The strategic point is clear here : ST is not exposed through a single product or partnership, but through multiple independent layers of the same architecture. Each core technology — power, cooling, photonics, and embedded processing — solves a different bottleneck that modern AI systems cannot avoid.

The Orbital Edge

The data-center opportunity is substantial, but evaluating ST only through that lens misses a second growth engine running in parallel :

ST supplies about 90% of the low-Earth orbit satellite semiconductor market including both Starlink satellites and the user terminals that connect to them on the ground. LEO revenue rose from $175 million in 2021 to $600 million in 2025, a 243% increase in four years, and is approaching $1 billion in 2026. Management has guided to well above $3 billion in cumulative space revenue between 2026 and 2028. This momentum is underpinned by a widening commercial footprint, highlighted by ST ramping high-volume shipments to its second-largest customer in the LEO satellite ecosystem.

The barrier protecting that position is not capital but physics and qualification time. Conventional silicon degrades quickly under cosmic radiation. ST’s radiation-hardened product lines are designed specifically for space, and qualification takes years. Even if a competitor outspends ST to copy this architecture, because you cannot buy a decade of proven orbital reliability, ST’s dominant market share remains structurally protected.

With the SpaceX IPO anticipated and hyperscalers announcing satellite distribution partnerships, demand for orbital hardware is reaching an inflection point. ST is one of the few companies already positioned to benefit from it.

Financial Profile

ST’s financial profile reflects a company navigating a multi-speed operational recovery :

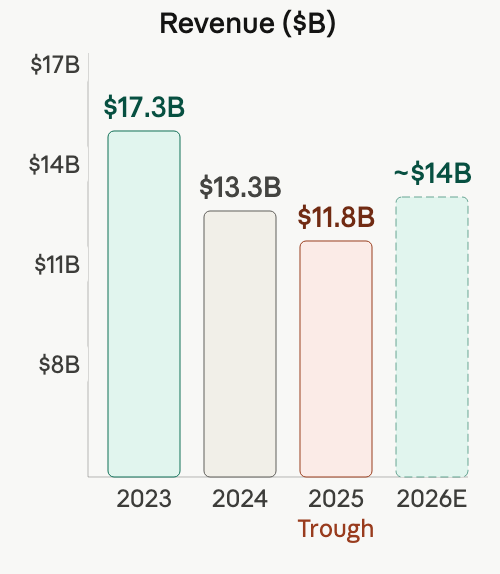

The historical automotive and industrial legacy business completed its structural cyclical bottom in late 2025 following an extended post-pandemic channel inventory correction.

Concurrently, the high-margin AI infrastructure and orbital aerospace segments are entering an unconstrained growth ramp.

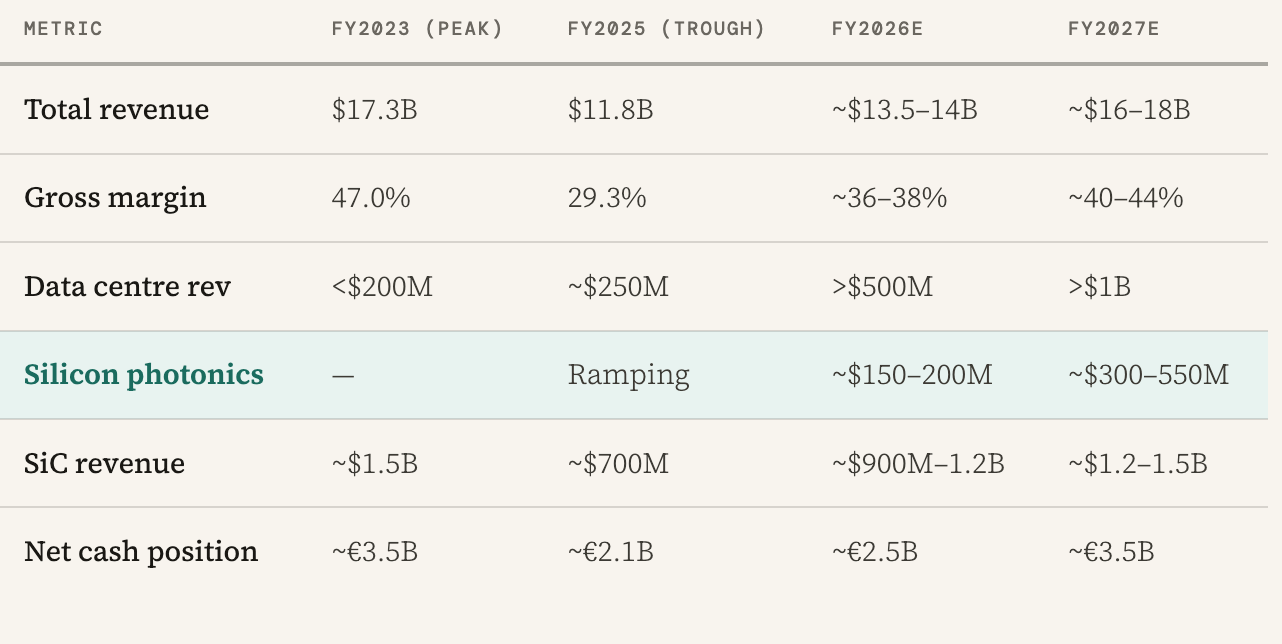

Full-year 2025 revenue settled at $11.8 billion, down from the cyclical peak of $17.3 billion achieved in FY2023, with gross margin compressing to 29.3% due to significant underutilization charges levied against its fixed-cost manufacturing facilities.

But ST’s Q1 2026 financial results already confirmed a structural pivot:

Q1 2026 Revenue: $3.10 billion, outperforming consensus expectations of $3.04 billion and delivering 23% year-over-year growth.

Blended Gross Margin: Sequentially recovered to 33.8%.

Q2 2026 Guidance: Management guided the subsequent quarter to $3.45 billion in revenue (an 11.6% sequential expansion) with gross margins advancing to 35.2%.

CFO Lorenzo Grandi confirmed that gross margins are modeled to expand sequentially through every quarter of FY2026, with a clear path back above the 40% threshold as corporate quarterly revenue approaches a normalized run-rate of €4 billion.

The structural contribution of the data center segment is now clearly visible within the company’s financial modeling. CEO Jean-Marc Chery confirmed that data center vertical revenues are on track to exceed $500 million for full-year 2026 and are modeled to surpass $1 billion in FY2027 :

This revenue stream is split in a balanced 40/60 ratio between high-power analog architectures and the micro controller photonics segment, with photonics tracking as the fastest-growing sub-segment.

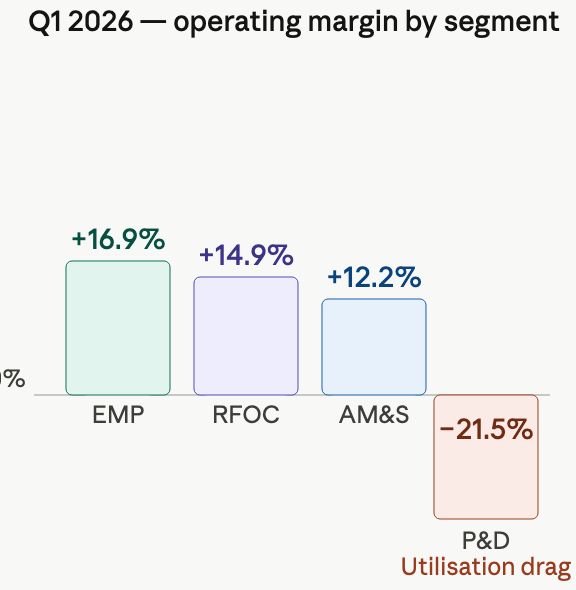

The segment breakdown shows why the margin recovery matters.

The Power & Discrete (P&D) segment posted an operating margin of –21.5% in Q1 2026 and –16.3% for full-year 2025. On the surface, this looks alarming. In practice, it is almost entirely an accounting artefact.

STM operates capital-intensive fabs with large fixed cost bases. When those fabs run below capacity, the unabsorbed fixed costs are charged directly to the P&L as “unused capacity charges.” In FY2025, those charges totaled $416 million — equivalent to roughly 25% of the entire P&D segment’s revenue. Strip those out alongside one-time restructuring costs and the segment’s normalized margin is closer to +13%, not –16%.

This operational transition is protected by a conservative balance sheet. ST concluded Q1 2026 maintaining a net cash position of approximately €2.0 billion, backed by total available liquidity of €4.57 billion. This capital position has allowed the firm to consistently self-fund its multi-billion-dollar fabrication expansions in Catania and Crolles through cash flow without accumulating dilutive high-interest debt, preserving financial flexibility through the bottom of the semiconductor cycle.

The Valuation Case — Two Parts

Part I: P&D Recovery Drives the Re-rating

To understand where ST’s valuation is headed, start with what is holding it back today.

The main issue is gross margin, which is being dragged down by one segment: Power and Discrete (P&D). In Q1 2026, P&D reported an operating margin of −21.5%. This is not a technology issue — it is a utilization problem.

ST built its Catania SiC campus for an EV market growing at 30–40% annually. When EV demand slowed, volumes dropped, but the fixed costs of the facility remained. Those costs are now spread over much lower revenue, hurting margins. The accounting looks weak, but the asset itself is highly valuable and difficult to replicate.

The recovery in P&D is already underway, driven by five clear factors:

First, the ramp of 800V AI data centers. ST is on Nvidia’s approved supplier list for its Kyber architecture. Management expects data center revenue to exceed $500 million in 2026 and $1 billion in 2027. About 40% of this is power and analog (SiC and GaN), directly replacing lost EV demand. As volumes increase, the same underutilized capacity becomes profitable.

Second, LEO satellite demand. ST expects over $3 billion in cumulative space revenue from 2026 to 2028, or about $1 billion per year, with very high margins. The company holds roughly 90% market share, supported by years of radiation-hardening expertise. This is stable, high-value demand that fills unused capacity but is largely missing from current models.

Third, the Huahong partnership. ST has begun delivering STM32 wafers produced in China. This lowers unit costs and improves efficiency across its microcontroller business, with increasing benefits as volumes grow.

Fourth, the Physical AI collaboration with Nvidia. ST’s microcontrollers and sensors are being designed into robotics and industrial systems. This creates another source of high-volume, high-margin demand using existing capacity.

Fifth, strong order momentum. Book-to-bill was above 1.0 across all markets and regions in Q1 2026, indicating broad demand. Q2 revenue is guided to $3.45 billion (up 25% year-over-year), with double-digit growth expected for the full year.

When these factors are included in a forward model, the financial outlook changes significantly. Here is my assumption :

P&D operating margin improves to around 12% as unused capacity costs fall from $416 million in 2025 to about $25 million by 2027.

Data center revenue exceeds $1.1 billion.

LEO satellite revenue exceeds $1.2 billion.

Group EBIT margin reaches about 20% on roughly $17.7 billion in revenue.

At a valuation of 16× EV/EBITDA — and a price-to-book of 3.2×, this implies meaningful upside from current levels :

The key point is operating leverage. Moving P&D from −21.5% to +12% operating margin on about $1.6 billion in revenue adds roughly $0.50–0.55 per share in earnings. Current 2027 consensus EPS of $1.82 does not include this improvement. When it shows up in reported results, estimates will adjust quickly.

Based on this, here is my valuation model :

The financial story is catching up to the strategy — but the market has not fully recognized it yet.

Part II: Why the Multiple Could Expand Further

P&D recovery explains earnings growth. It does not fully explain why ST could trade at a higher valuation multiple.

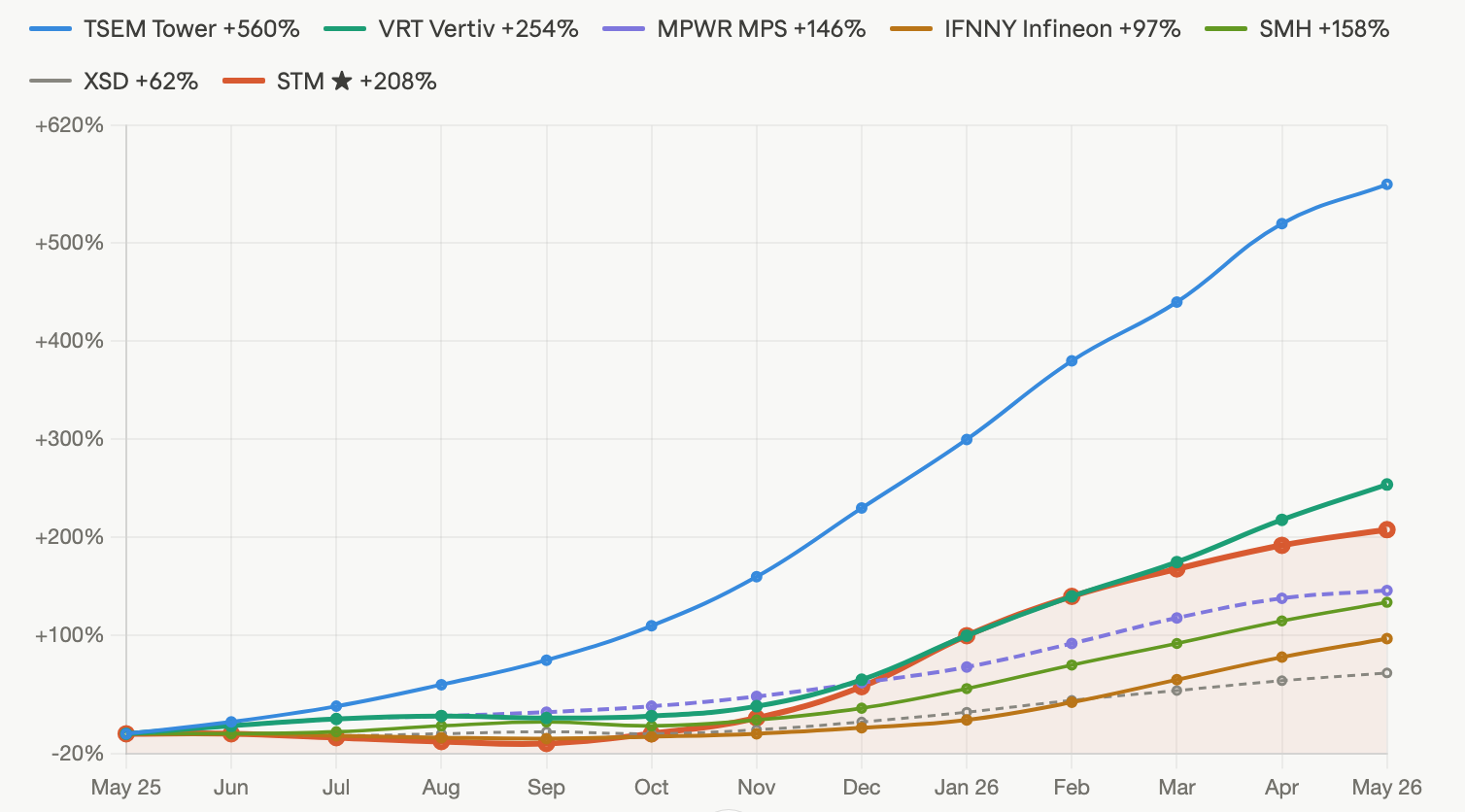

Over the past year, markets have rewarded companies solving key AI infrastructure bottlenecks: During the twelve months from May 2025 to May 2026 price action were sharp, consistent, and tied directly to thesis simplicity :

This chart is indexed to 0 in May 2025, and the companies were deliberately chosen to provide a clear comparison across AI infrastructure, direct peers, and the broader semiconductor sector.

Vertiv rose +254% with almost no pause: AI racks generate extreme heat, and Vertiv removes it. Thermal bottleneck. Obvious solution. Relentless re-rating.

Tower Semiconductor gained +560% — the group’s strongest move — because copper fails at AI data rates and Tower builds the photonic engines that replace it. Once $1.3 billion in 2027 contracts and $290 million in customer prepayments confirmed the story, the re-rating accelerated strongly.

Monolithic Power Systems rose +146% as the market recognized that next-gen GPUs demand power delivery legacy chips can’t handle. MPS supplies the power management silicon directly beneath the GPU. Enterprise data revenue nearly doubled; the stock followed.

Infineon gained +97%, but not linearly. It declined through most of 2025 alongside ST until a single catalyst — a patent ruling and guidance raise — simplified its complex industrial story into something the market could quickly price.

SMH returned +158%, driven by Nvidia; XSD gained +62%, reflecting the average chip stock that saw no full re-rating. The benchmarks show how high the tide rose — and how selectively.

ST rose roughly +208% over the period, a solid recovery that must be read correctly. The stock was still falling in May 2025, hit a low of $21.11 in November, then rebounded to ~$65 by May 2026. That ~+208% recovery from the trough is real and rapid, but I believe it reflects removal of an extreme automotive-downside discount, not a full re-rating as an AI infrastructure company. This distinction matters: it’s a recovery, not a re-rating. The penalty is gone; the premium hasn’t been applied fully.

This mismatch has created a valuation gap. The market has handed out 50x–90x multiples to simple, single-variable plays — pure-play cooling or standalone power modules — yet assigns ST a conservative 35x forward earnings multiple, even though it supplies the foundational silicon enabling those layers.

I see here a “complexity discount” punishing somewhat the stock because its multi-layered business is hard to model. But as these deep-tech segments begin reinforcing one another in upcoming quarters, I think the discount will evaporate.

Investors tend to re-rate companies when a single, clear metric simplifies the narrative : For ST, that metric is data center revenue.

At that point, ST will be seen as a multi-domain AI infrastructure company rather than a cyclical auto supplier.

When that shift happens, the current multiple may no longer hold.

The recent re-rating cycle has rewarded memory, Semi conductors but has not yet reach Interconnection. This is where ST navigate : a technically critical company operating across multiple layers, but not yet fully understood.

The complexity discount is real, but it tends to disappear quickly once the market aligns on the narrative.

Risks

Automotive Macro Disruption: If the European automotive sector experiences an extended structural contraction — driven by decelerating consumer EV adoption rates, aggressive market share capture by Chinese OEMs within continental Europe, or broader macroeconomic tightening — underutilization charges within the P&D segment will persist longer than current recovery models assume, capping near-term gross margin expansion.

Silicon Photonics Yield Vulnerabilities: While the PIC100 platform is actively running volume production for AWS, silicon photonics manufacturing involves complex lithographic alignment steps that render its yield ramp structurally more volatile than traditional digital CMOS processes. Any stalling in yield optimization at the Crolles facilty will elevate unit manufacturing costs and defer the projected revenue ramp.

Silicon Carbide Price Erosion: Competitors, most notably Onsemi, are pursuing aggressive pricing strategies to secure long-term capacity agreements with tier-one automotive manufacturers. If wide-bandgap markets devolve into a commoditized price war before data center demand fully absorbs global capacity, ST’s internal margin protections will be partially compromised.

Single-Source Photonics Substrate Reliance: The PIC100 platform depends on highly specialized Photonics-SOI (Silicon-on-Insulator) engineered wafers single-sourced from French materials firm Soitec under proprietary patent monopolies. Any operational disruption or supply chain constraint at Soitec’s facilities represents a single point of failure that would immediately block ST’s optical engine production.

Closing Thought

STMicroelectronics is not a newcomer staking a claim. It is an industrial institution that has spent decades laying the physical groundwork for high-consequence computing and global communications. The opportunity is not entirely undiscovered, and the initial upgrades are already under way.

What analysts fail to grasp, however, is that ST holds a definitive, yet largely unrecognized, moat in the new economy : AI Interconnection. To see its true value, you have to move past standard piece-meal analysis and look at the whole architectural approach. ST is not a single-component vendor hoping for a generic macro turn. It is a fully vertically integrated, sovereign powerhouse that simultaneously touches multiple critical layers and control the movement of the AI stack. By owning the entire lifecycle—from raw substrate to finished silicon—ST directly has an ecosystem of products aiming to resolves the hard physical bottlenecks of power, connectivity, and thermal limits that modern AI simply cannot bypass.

When you step back and evaluate this total infrastructure readiness against the current geopolitical and technical landscape, ST’s position is remarkably well-fortified.

The physical bottlenecks of the AI era touch every layer of the computing stack, and ST is confirmed across all six simultaneously. But the deeper point is what connects those layers: light, energy, and localized intelligence — the three physical materials without which no AI system can function, and the three things ST manufactures at industrial scale in owned sovereign Western fabs.

In the Age of Interconnection, whoever controls the connections controls the era. ST does not merely sit at the layers. It is the connections.

Disclaimer: This article is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. The author may hold positions in securities mentioned. All data sourced from public company filings, earnings transcripts, and analyst research available as of May 2026. All investment decisions are the reader’s own responsibility.

Intéressant !

Thanks Louis, more to come!